A defective system

There is something terribly wrong with this system, isn't there?

So you think that money is the root of all evil. Have you ever asked what is the root of all money?

In the chapter What is money?, we saw some historical examples of money and some properties that good money should have. Unfortunately looking at money through history, and what properties money should have, is not enough to understand the current economic system, which is a completely different beast.

As we saw in the previous chapter, a big problem is that our leaders don’t know how to steer this financial beast. But there are more problems to the modern system, again related to being based on unsound money where a flexible money supply breaks the properties of good money. This has far-reaching negative consequences and it means the economic system we use today is broken, on a fundamental level.

Economic effects of counterfeiting

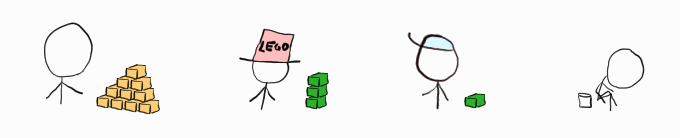

Imagine a counterfeiter, who has the ability to print money from thin air. What would he do with all the money? What would you do?

Personally, I would probably pay off my loans, renovate our house, go on vacation and buy a bunch of LEGO®. If I was smart I would also invest it; buy some stocks, some gold, maybe a house or two and rent them out. In short I would buy a bunch of stuff—and I think most would do the same.

If I did print money—a lot of money—and spent it like this, what would the effect on the economy be?

For starters, if I just kept the money without spending it, nothing would change:

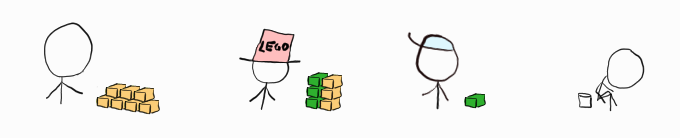

Then if I decided to buy a bunch of LEGO®, the store would get some of my money:

After a while the store would use the counterfeited money to pay their supplier:

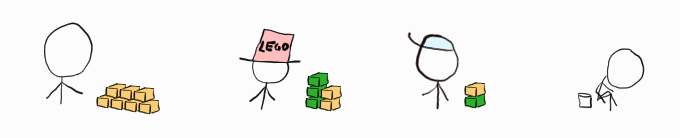

Who in turn will use it to buy other stuff, and in this way the counterfeited money slowly trickles out into the rest of the economy. This extra money has two important effects:

Higher prices.

Because there’s more money going around, with the same amount of goods, the prices will rise. For instance if all the money in the world would double overnight, then naturally all prices would double too. Yesterday’s $100 bill would today only get you $50 worth of stuff.

When prices rise and the same amount of money buys you less stuff, we call it inflation. It’s how my grandmother could buy candy for one cent (0.01 SEK) when she was a child, while today our smallest coin is 1 SEK.

Redistribution of wealth.

Notice how in our previous example the counterfeited money isn’t divided equally. The counterfeiter suddenly became much richer than everyone else, and some received a bit more than others. Notice that the poor guy to the right in the example—who had very little to start with—didn’t receive any money and became even poorer, relatively speaking.

Counterfeiting means everyone’s savings—the “old” money—will lose value. This is why you shouldn’t just store all your money as cash under the mattress or in a bank account—the value will be eaten up by inflation.

How the inflation in Sweden has caused the actual value of money to decrease.

The graph shows an inflation adjusted index, starting from 1960. You can think of it what 100 SEK of goods in a given year would be worth in 1960’s money. For example 100 SEK from 2018 would only buy 7 SEK worth of stuff in 1960—a 93% drop in value.

You can also compare two years with each other. For example the index in 1976 was around 40, and in 1982 around 20, which means money lost 50% of its value between 1976 and 1982.

Counterfeiting redistributes wealth from everyone to the counterfeiter (and to a lesser extent people the counterfeiter buys from) at the same rate as the inflation eats up the value of money. Even though nobody’s stealing your money, the effect is the same: your wealth relative to others will decrease.

Legal counterfeiting

While I think most will agree counterfeiting shouldn’t be allowed, the modern economic system is built upon legal counterfeiting. There are entities who have the legal right to print money—with the same negative consequences on the economy that counterfeiting has. As noted earlier the central banks have this right, but regular banks can increase the money supply as well.

The central banks—the Federal Reserve (Fed) in the U.S. or the European Central Bank (ECB) in the EU—are the only ones allowed to print physical money. Which they have to do, if only to replace old bills.1 They also have an inflation target, usually 2% or 3%, meaning the goal is to devalue the money. The rationale is it drives economic growth because shoppers will buy now to avoid higher prices later.2

Although the central banks are ultimately responsible, it’s the regular banks who expand the money supply the most. It’s done via fractional banking which works like this:

In the beginning John has 1 000 SEK, with nothing strange going on. This is the balance sheet for John and the bank:

JohnBank1 000 SEKJohn lends the money to the bank, and receives money promises from the bank (let’s call them IOUs):

JohnBank1 000 IOU1 000 SEKThe bank can issue more IOUs if they want, here they lend out IOUs to Jane:

JohnBankJane1 000 IOU1 000 SEK9 000 IOU

There is now 11 000 money circulating the system. Because an IOU is treated like a SEK for all intents and purposes we can even say that there’s 11 000 SEK now after we started with only 1 000 SEK. The bank printed 10 000 SEK from thin air and has only 1 000 SEK to back them up. The ratio of SEK to IOU, in this example 10%, is called the reserve.

That’s as good as money, sir. Those are I.O.U.s.

We might wonder, why stop at only printing 10 000 SEK? Why not 100 000 SEK? Or more? When the bank gives out IOUs they do need to repay them, otherwise they’ll fail and become bankrupt. In the example above if Jane would withdraw 2 000 SEK the bank would fail, because it can only repay 1 000 SEK.

The system works as long as people just keep their money at the bank, and only occasionally withdraw their money. But if people start withdrawing a lot of money at the same time, a bank run may cause the bank to fail. To reduce this risk, banks have requirements on their reserves.

Lender of last resort

As money printers, the central banks play an important role—as the “lender of last resort”. This means when all else fails, for example if the banks are about to go bankrupt because they have too little reserves or if the economy is going bad, then central banks can step in and save them. As we saw in an earlier chapter this is exactly what happened during the 2008 financial crisis, where banks and other institutions messed up in a major way but were bailed out and made whole again.

This means the real check against fractional banking (the risk of going bankrupt) is thrown away and replaced with regulation that’s supposed to keep the banks in check, while making the banks more robust against failure. While fine in theory, in practice it means banks are now incentivized to push the limits any way they can, to maximize their profits.

I don’t think there’s a better example of the hazards the lender of last resort creates than the 2008 financial crisis. I feel the term moral hazard, to describe someone taking risks others will pay for, is too soft to describe the situation.

A crucial part of being the lender of last resort is to act as an overseer and to keep the banks in check. But as Fed whistleblowers show, the Fed acts less like an enforcer and more like a kind grandpa, silencing examiners to help the banks look good:

In a tense, 40-minute meeting recorded the week before she was fired, Segarra’s boss repeatedly tries to persuade her to change her conclusion that Goldman was missing a policy to handle conflicts of interest. Segarra offered to review her evidence with higher-ups and told her boss she would accept being overruled once her findings were submitted. It wasn’t enough.

Reason behind the madness

If you’ve followed along this far, you might get the feeling that the economic system is completely corrupt and wonder why anyone would ever get along with it? But not so fast—there’s a reason things are the way the are, and a big part can be traced the Great Depression in the 1930s.

The Great Depression was a huge economic crisis, the worst in modern history, that dwarfed the 2008 financial crisis. Experts debate the causes of this decade long crisis to this day, with explanations ranging from governments spending too little, printing too little money, printing too much money or the gold standard.

While it’s difficult to point out causes, and it’s even debatable why we got out of it, it’s fairly easy to point out some big changes introduced when combating the crisis:

Abandoned the gold standard

After briefly dropping the gold standard to pay for World War I, all countries left the gold standard during the depression.

Proactive governments

In the New Deal the United States tried to stimulate the economy by for example building infrastructure, building houses, paying farmers to plant crops, producing power and insuring loans.

Debt fueled investments

To pay for these investments the United States greatly increased their debt from $22 billion to $40 billion.

These align with the ideas of Keynesian Economics (also developed in the 1930s) where governments should stimulate the economy during recessions, and compensate by pulling back when the economy’s expanding. The rationale is that the velocity of money (how fast companies and people spend money) will slow down during a recession, making it worse. Therefore the government should increase their spending—increasing the velocity of money—to help dampen the recession.

Seen through this lens, it all makes sense. To help the government spend money it doesn’t have, being able to print money is a huge help. When the government goes deeper into debt, again it helps to be able to print money. And the interaction between central banks and banks is a fairly efficient way to setup a money-printing machine.

A mountain of debt

While taking out debt to fuel investments was only supposed to be a temporary measure to help the economy during downturns, today we massively increase the debt all the time. For example we’ve seen a record bull run in 2009–2019, yet the U.S. debt doubled from $11 trillion to $22 trillion during the same period.

After the 2008 financial crisis the amount of debt skyrocketed, signifying a shift in economic policy.

During the COVID-19 pandemic the debt explosively increased at a pace unseen before.

Taking out a loan essentially borrows money from the future you, since you have to pay it back with interest. And the U.S. is paying for that now: in the 2020 budget 10.1% is spent on only the interest rate, and it’s expected to take up 12.9% in 2026, making it the fastest rising expense in the budget. Most of the debt is public debt (debt to people, companies or other governments), so refusing to pay would have disastrous consequences.

Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it.

This isn’t a situation unique to the United States, but a global phenomena. While the U.S. has a national debt at 104% of GDP (a way to compare relative debts between countries), Sweden has a debt of 38%, Germany 61%, Italy 132%, Greece 181% and Japan a staggering 235%.

It seems like we’re moving away from the original Keynesian ideas to something else, where paying off national debt matters less as we can just print more money.

Growing inequality

It doesn’t matter if you’re black or white… the only color that really matters is green.

There’s a worrying trend in the world: global inequality is rising. The rich get richer and the poor get… poorer.

Source World Inequality Database.

The inequality is on the rise in nearly every country. If we take a closer look at the United States, it paints a gloomy picture:

Source World Inequality Database.

Source World Inequality Database.

While the money-making machine isn’t the only cause of the inequality, it’s a pretty difficult situation to reverse when even the national economy works against you. Printing money to solve problems will, in line with the previous counterfeiting example, only fan the flames and make the situation worse.

No tools left

We want to pull back on stimulation when the economy is booming, so we’re prepared with all our tools when the economy is crashing. Unfortunately after a decade of economic boom, we’ve done the opposite:

The national debt has skyrocketed

The larger the debt, the more expenses must be devoted to repaying the debt, leaving less for other more useful things.

The central bank interest rates are already low

A low rate means banks, and in extension we, can get cheaper loans which stimulates the economy. It’s difficult to lower it more when it’s almost zero, or even negative, already.

We’re continually printing money

The Federal Reserve is pouring money into the financial system. Printing an unlimited amount of money isn’t great, not only because of the erosion of wealth, but rampant inflation can quickly destroy the economy.

To be fair, the Federal Reserve knows this isn’t an ideal situation, so they tried to raise interest rates. Unfortunately, the stock market reacted poorly—many people got angry—and now they’ve backtracked and lowered them again. When problems arise, they use the financial equivalent of taking a sledgehammer to squash a bug.

So, we’re stuck in a situation where we don’t have the tools to defend against a recession—tools the economic theory the system is built on needs. Tools that have been used up, because that’s what the theory says we should do.

It seems to me if (or when) a recession comes we’ll get caught with our pants down. And things have been looking pretty shaky a while now.

The stock market magic trick

When the world locked down during the COVID-19 pandemic the economy predictably crashed. Many people (including me) thought that the big recession was finally here and we’d be looking at several years of tough times.

But then something weird happened. Despite entire cities and countries locking down; the number of unemployed reached record numbers and many smaller companies closed their doors for good, the recession didn’t come. Instead the stock market recovered very quickly, as if closing down the world economy was just a minor speed bump.

One might wonder, what the hell happened?

The Federal Reserve followed the script and printed trillions of dollars and used it to prop up the stock market. As seen in the M2 graph this was an extreme amount of money in a very short period of time:

M2 is a measure of money supply that includes cash, checking deposits, savings deposits, money market securities, mutual funds and other time deposits.

Unfortunately the money printing didn’t help the businesses that went out of business or the people who became unemployed. The money was instead funneled to the big companies who used it to artificially increase their valuation with stock buybacks or just placed the money in their reserves. The money didn’t trickle down to the masses; it got stuck driving up the stock price.

Nothing fundamentally changed. The deep-rooted economic problems are still there, festering.

Where do we go from here?

Since the financial crisis in 2008 we’re in uncharted territory, and we actually don’t know what we should do. Therefore new economic theories, like the Modern Money Theory (MMT), are developed. MMT basically says the government can pay its bills by just printing all the money it needs, checked only by inflation. It’s reasonable to ask if MMT is a sound economic theory, or if it’s just describing what’s already happening.

While “printing more money” is a popular solution, sound money (with a stable money supply) might represent a compelling alternative for critics of the modern economic policies. For example fiat backed by gold, actual gold coins or cryptocurrencies.

It’s not easy to see how a switch to sound money would occur and such a switch may likely introduce more problems than it solved. However, it would mean that manipulation of the money supply would disappear; that we wouldn’t accumulate a mountain of debt; that we wouldn’t devalue our savings while increasing the wealth inequality; and that we wouldn’t cling to the broken and defective economic theories in use today.