For the unbanked

Digital payments for those without a bank account

A growing body of research reveals many potential development benefits from financial inclusion—especially from the use of digital financial services, including mobile money services, payment cards, and other financial technology (or fintech) applications.

In the previous chapters we’ve looked at some problems with having to get permission to accept digital payments, and what happens when we don’t. This time we’ll look at the reverse problem: when you can’t make digital payments.

To make digital payments, you typically need a bank account and those without one are often called unbanked. Paying bills digitally, using credit cards and even mobile payments all require a bank account. If you don’t have a bank account, you’re essentially shut-out from the digital economy.

The problems the unbanked face are difficult to solve, and cryptocurrencies won’t magically solve them all, but if adopted they can be helpful.

Who are the unbanked?

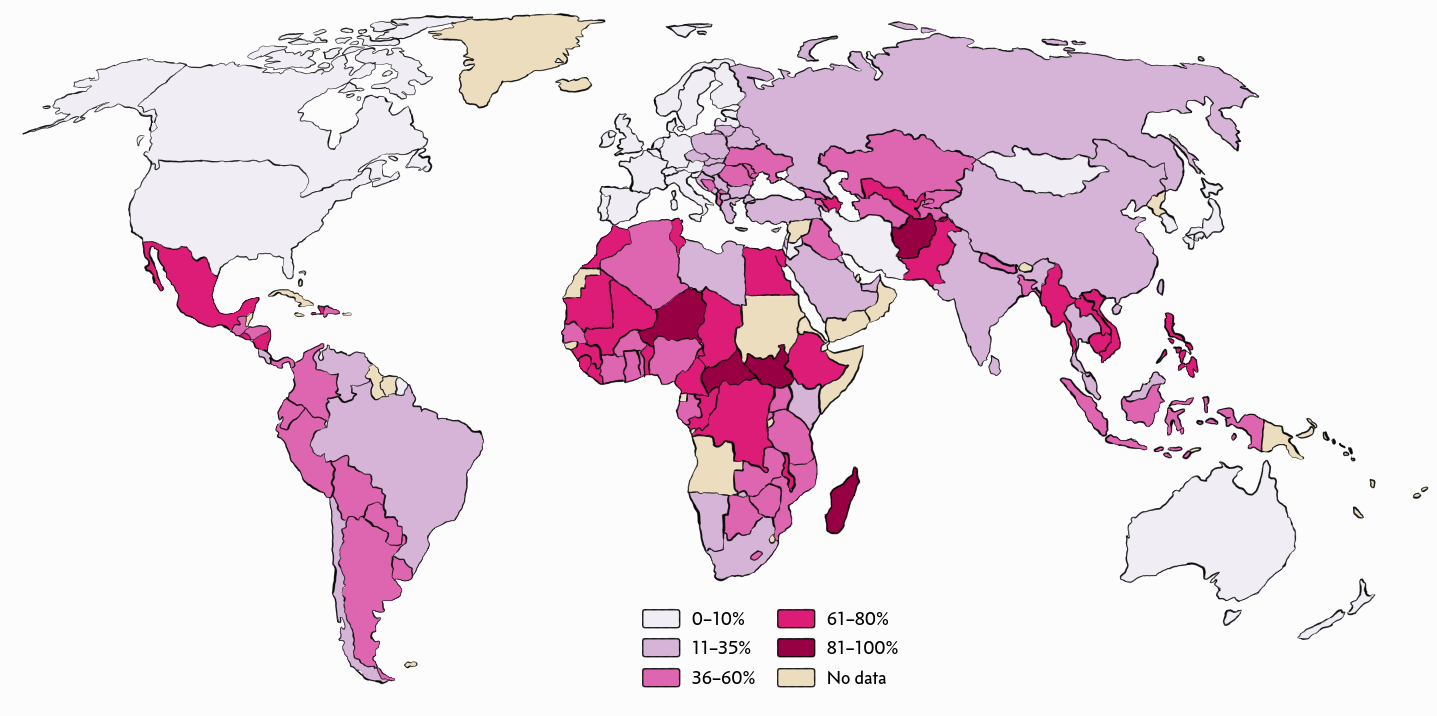

There are 1.7 billion adults without a bank account in the world. To get a sense for what countries they come from, take a look at this world map:

Source Global Findex database.

This map helps us identify countries with a high fraction of unbanked and we can for example see that it’s common to be unbanked in Africa and in South America but uncommon in western Europe and the Nordic countries.

The unbanked are in general less educated, where 62% of unbanked only have a primary education or less, compared to around half overall in developing economies. Twice as many unbanked people live in the poorest households as in the richest ones and 56% of all unbanked are women.

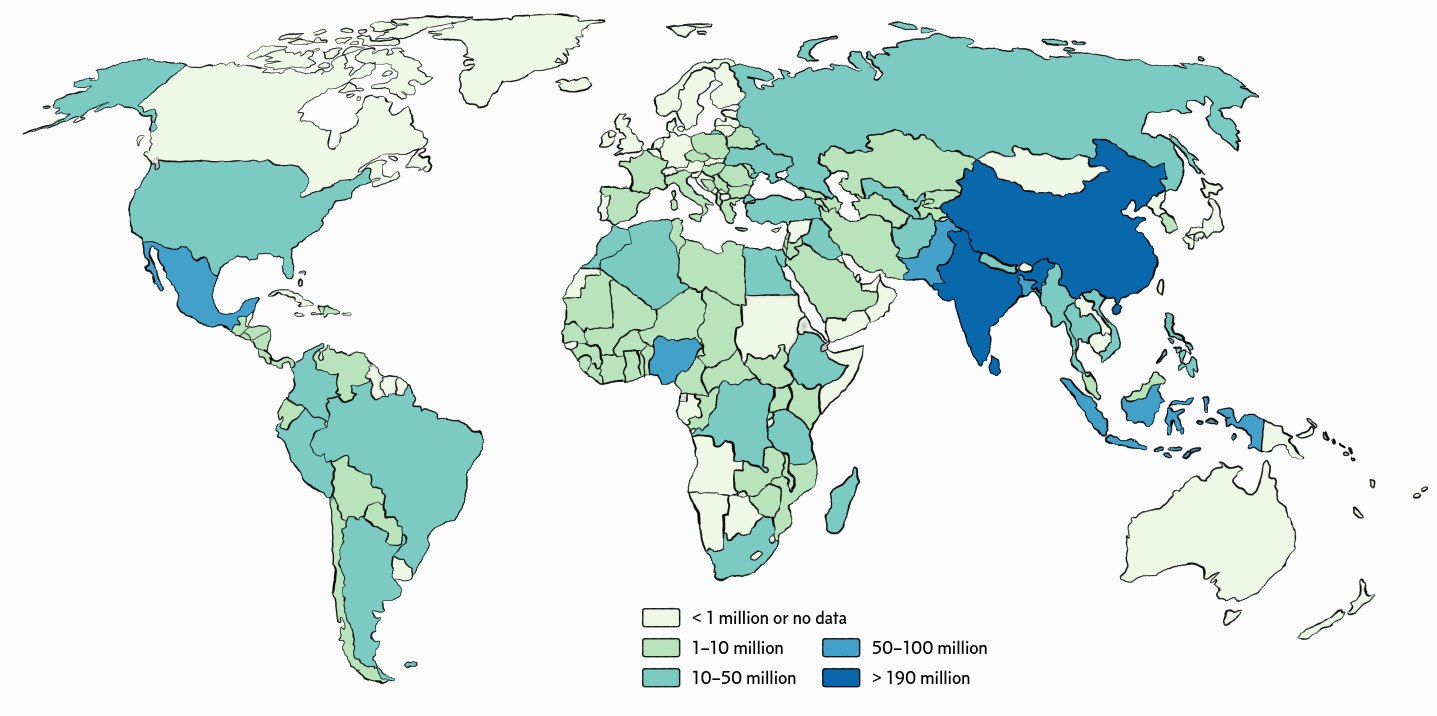

Another way to look at the world is to visualize the raw number of unbanked in every country, which shows us where the 1.7 billion unbanked come from:

Source Global Findex database (interactive).

Almost half of all unbanked people live in just seven countries: China, India, Indonesia, Mexico, Nigeria, Pakistan and Bangladesh. In fact China (224 million) and India (191 million) alone make up nearly a quarter of all unbanked in the world.

While the fraction of unbanked adults are high in the developing countries with poor access to electricity and internet, a surprisingly large number of unbanked also live in developed countries. For example USA has 18 million unbanked and in France there are 3 million unbanked.

Why are they unbanked?

The Global Findex database also tried to examine why people stay unbanked:

Source Global Findex database.

The most commonly cited barrier was not having enough money. Around 60% said they had too little money to use a bank account, with almost 20% citing it as the sole reason.

Most cite several different reasons, making it hard to rank the issues in importance. For example many say they don’t need an account, but if the other barriers were to disappear they might find accounts useful if only they had access to them. At least this gives a sense of what issues are present.

Unbanked with internet

The question “But how do the unbanked pay for internet?” is always asked when discussing the unbanked. The report has this to say:

How many unbanked adults have a mobile phone? Globally, about 1.1 billion—or about two-thirds of all unbanked adults. In India and Mexico more than 50 per-cent of the unbanked have a mobile phone; in China 82 percent do.

Fewer unbanked adults have both a mobile phone and access to the internet in some form—whether through a smartphone, a home computer, an internet café, or some other way. Globally, the share is about a quarter.

So about 420 million do have access to internet while being unbanked. I don’t know if that’s true or not, but anecdotally it seems almost all homeless people I’ve seen own a smartphone of some sort. You can even get internet in Venezuela, despite an unreliable power grid. And consider that even rich and successful people can become temporarily unbanked, for example if banks arbitrarily decide porn stars and marijuana supporters aren’t something they want to be associated with.

What’s the problem?

There are two big problems with being unbanked related to digital payments as I see it, one on a country level and one for individuals:

- Countries miss out on economic growth.

- Individuals may be shut-out from society.

Economic growth

Continuing the quote from the beginning of the chapter:

The benefits from financial inclusion can be wide ranging. For example, studies have shown that mobile money services—which allow users to store and transfer funds through a mobile phone—can help improve people’s income earning potential and thus reduce poverty.

A study in Kenya found that access to mobile money services delivered big benefits, especially for women. It enabled women-headed households to increase their savings by more than a fifth; allowed 185,000 women to leave farming and develop business or retail activities; and helped reduce extreme poverty among women-headed households by 22 percent.

One of the best ways to fight poverty is economic growth. This is fairly undisputed, although the link may be indirect. As I see it, convenient digital payments contribute to economic growth in two ways:

Increased economic efficiency.

Since digital payments allow for more convenient payments, especially over longer distances, they increase the efficiency in the economy leading to economic growth.

A cornerstone for inclusion into the ever-more digitalized world.

Globalization, or how the world has become more interconnected, has been a theme in the last century or two. It has never been easier to travel to the other side of the world, to talk to them over the internet or have them ship goods to you for very low fees.

If people don’t have access to digital payments the country risks becoming more isolated and might miss out on the economic growth caused by globalization. (Of course there are downsides with globalization as well, just look at the trade war between the U.S. and China).

Shut-out from society

It might be relatively fine for you to live in a country without a bank account—as long as others don’t use one either. But what if you live in a country where digital payments are an integral part of society?

For example here in Sweden almost everyone and everything uses digital payments. It would be extremely difficult for you to live here without a credit card or a bank to pay your bills.

One time when I went on a small business to the middle parts of Sweden, I accidentally forgot my wallet, including my credit cards and identification card. I borrowed some cash from a friend, thinking I could use them to pay for lunch and dinner, but surprisingly most restaurants didn’t accept cash. So, I still had to ask my co-workers to pay for me…

I don’t really know how people without a bank account manage in Sweden or what tourists will do if their credit card stops working? With the current development, they might not even be able to use public bathrooms!

In China, mobile payments are growing like mad. If you’re a tourist, you should get them, otherwise you’ll have a tough time. This in combination with China’s social credit, which ranks people’s behaviors to make sure they’re in line with the party, is a recipe for disaster. If you score badly, you might not be allowed to fly and maybe you’ll lose the privilege of using digital payments.

What might cryptocurrencies help the unbanked with?

Of course “just use cryptocurrencies” isn’t the answer to all problems for the unbanked. Cryptocurrencies won’t magically give poor people money, make them educated and they can’t even completely replace banks. But it is a helpful tool which, as adoption grow, might be helpful for many without bank access.

There are a number of benefits cryptocurrencies have:

Cryptocurrencies are for everyone.

Cryptocurrencies are permissionless: you don’t need permission from anyone to use them. It doesn’t matter if you’re homeless, a porn star or a tourist—you can always have access to digital payments and you cannot be shut-out.

There is no KYC process.

Because cryptocurrencies are permissionless there’s no Know your customer (KYC) process, which banks are required to perform. That’s good for people who might not have proper documentation such as ID-cards or birth certificates.

The fees are low.

There are no fees for opening or having an account—like with traditional banks—and there are no KYC associated costs. There is only a small transaction cost you pay when using a cryptocurrency.

You don’t need to trust a third-party with your money.

In countries with high corruption you might not trust your local bank enough to handle your money. With cryptocurrencies you can hold your money yourself and there’s no need for a third-party to use it (such as a bank making the payment for you).

There’s no need to visit a financial institution.

As long as you have internet access you always have access to your money and can make payments. Getting started is as simple as installing an app on your phone.

These are directly related to the reasons why people stay unbanked, many of which cryptocurrencies might help solve. For example, the 30% who say bank accounts are too expensive and the 20% who say they lack documentation, may find cryptocurrencies a viable alternative as it is much cheaper than bank accounts and they don’t require any documentation. Cryptocurrencies also remove the requirement of having to trust a bank, which 15% of the unbanked cited as a reason for not having an account.

These benefits makes it possible for the 420 million unbanked who have internet access to use cryptocurrencies and gain access to the global economy.